Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment. Take 2 mins to learn more.

Ingenious Estate Planning Classic & Care Service 2025 Rights Issue

Please note that the availability of Business Relief from Inheritance Tax and Investors’ Relief for capital gains tax will be subject to the changes announced in the Autumn 2024 budget.

Important notice – offer now closed

The Ingenious Estate Planning Limited Rights Issue offer closed 5pm, Wednesday, 17 December 2025. The issue of the Rights Issue Shares is expected to take place by 15 January 2026, or earlier if practicably possible over the Christmas Period.

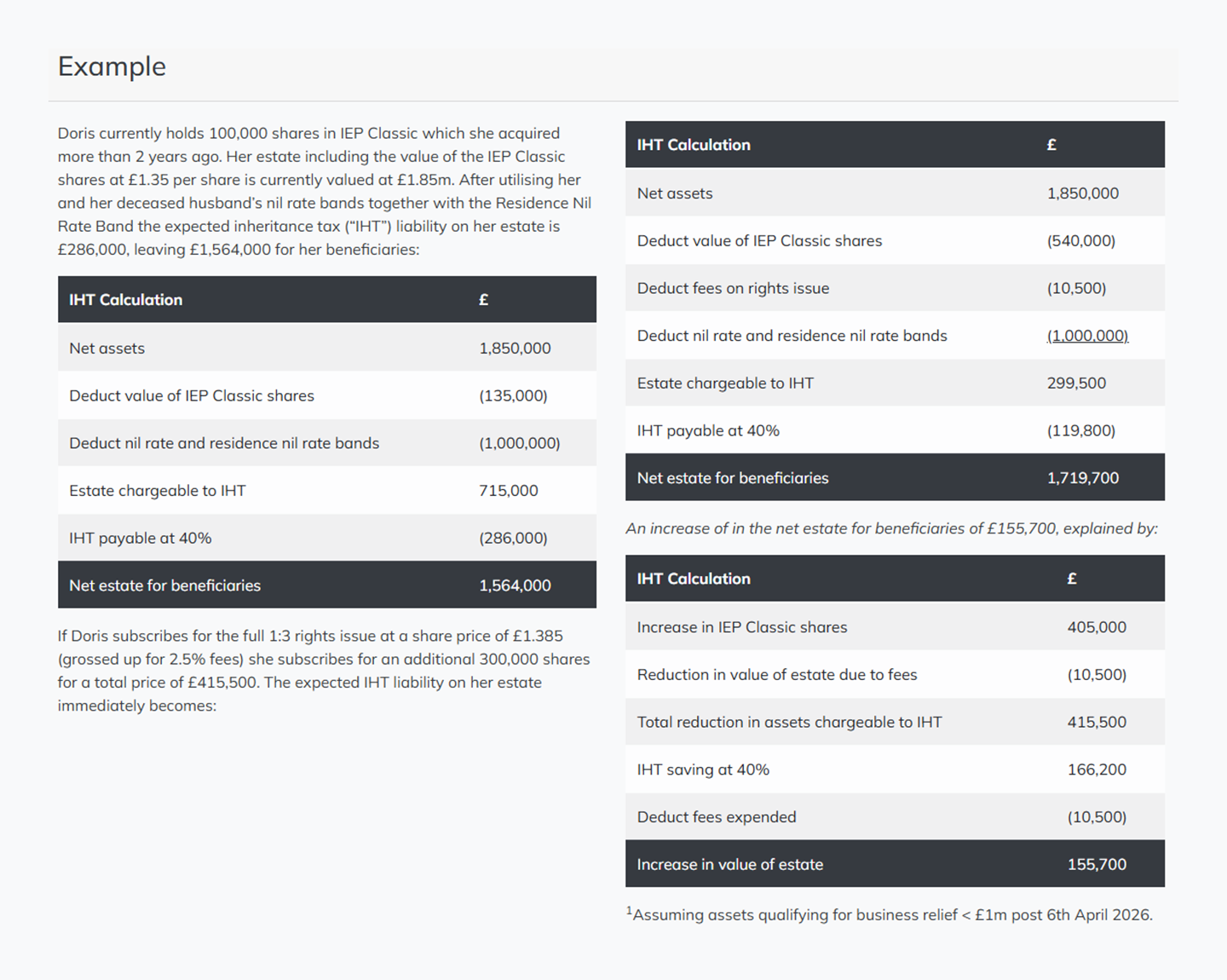

We’re offering existing shareholders in Ingenious Estate Planning Classic & Care (the “Services”) the opportunity to invest further through a “Rights Issue” – a chance to buy additional shares that may immediately qualify for Business Relief.

FAQs

Why subscribe for additional shares?

The new shares obtained under the rights issue (“Rights Issue Shares”) will qualify for Business Relief (BR) immediately if the original shares have already been held for 2 years at the date of the rights issue and the company issuing the shares is a trading company or the holding company of a trading group.

Applications can only be made through an authorised financial adviser. We do not accept applications directly from retail investors. You should speak to your adviser to determine whether this investment is appropriate for your individual circumstances.

More information about the potential benefits and risks can be found in the Ingenious Estate Planning Limited Rights Issue Prospectus, IEP Classic Brochure, IEP Classic Investor Agreement and Rights Issue Application Form.

There is no guarantee that shares issued to you will be wholly or partly Business Relief or Investors’ Relief qualifying at the date of a future transfer of your shares. Tax rules could change in the future and the value of any tax relief will depend on your personal circumstances.

Important information

Past performance is not a guarantee of future returns. As with any investment, there are inherent risks involved in investing in any of our products and money invested may both increase or decrease in value and your capital is at risk. There is no guarantee that you will be repaid all of your invested capital.

No Ingenious Group company provides or is authorised to provide investment or tax advice.